Introduction

Life can be unpredictable, and unexpected financial challenges can leave even the most responsible individuals overwhelmed by debt. For many South Africans, debt review is a beacon of hope, offering structured debt help to navigate through financial turmoil. But when is the right time to enter the debt review process? Understanding the signs of over-indebtedness and knowing when to seek assistance is the first step toward financial freedom.

This article explores the right moment to initiate debt review, what happens if you’re not considered over-indebted, and why now is always the best time to start your journey toward becoming debt-free.

Time to Initiate Debt Review

The debt review process is designed to assist consumers who are struggling with over-indebtedness, but the timing of when to initiate it is critical. The ideal moment to enter debt review is when your monthly debt repayments have become unmanageable and you’re unable to meet your financial obligations. The earlier you act, the more options you’ll have to prevent a financial crisis.

Signs You Should Consider Debt Review:

- Falling Behind on Payments: You’re consistently late on repayments or skipping them altogether.

- Borrowing to Cover Basics: Taking out loans to pay for essential living expenses is a major red flag.

- Creditor Pressure: You’re receiving letters of demand, phone calls, or legal notices from creditors.

Debt review offers a legal shield against these pressures, ensuring that creditors cannot take further action while you’re under the process. By restructuring your debt into affordable monthly payments, you’ll gain breathing room to focus on regaining control.

Unsuccessful Result if Not Over-Indebted

Not everyone who applies for debt review is deemed over-indebted. The National Credit Act (NCA) requires a comprehensive assessment of your financial situation by a registered Debt Counsellor to determine eligibility. If your income and expenses indicate that you can meet your debt obligations, you may not qualify for the process.

What Happens if You’re Not Over-Indebted?

- Rejection Notification: If the Debt Counsellor finds you are not over-indebted, you will receive a formal letter rejecting your application for debt review. You will then exit the debt review process and all debt review flags on your credit record will be removed.

- Explore Alternatives: In such cases, your Debt Counsellor may advise on other strategies, such as creating a budget plan, debt consolidation, or negotiating directly with creditors.

- Reapply When Needed: If your financial circumstances change—for example, due to job loss or increased expenses—you can reapply for debt review.

While being turned away may seem discouraging, it’s a sign that proactive measures, like improving your spending habits, can help you avoid falling into deeper debt.

Struggling to Make Ends Meet: Defaulting on Payments

For many South Africans, financial struggles become apparent when monthly budgets no longer balance. Missing payments or falling into arrears is often the first visible sign of over-indebtedness. This is the point where debt relief options, such as debt review, become crucial.

How Defaulting Affects You:

- Legal Action: Once you default, creditors may issue a letter of demand or even take legal action, such as garnishing your wages or repossessing your assets.

- Credit Score Impact: Missed payments negatively impact your credit record, making future borrowing more expensive or impossible.

- Increased Financial Strain: Penalties, late fees, and higher interest rates can quickly compound, worsening your financial position.

By entering debt review before defaulting, you can prevent these consequences. Even if you have already fallen behind, the process can provide immediate relief by halting legal proceedings and creating a manageable repayment plan.

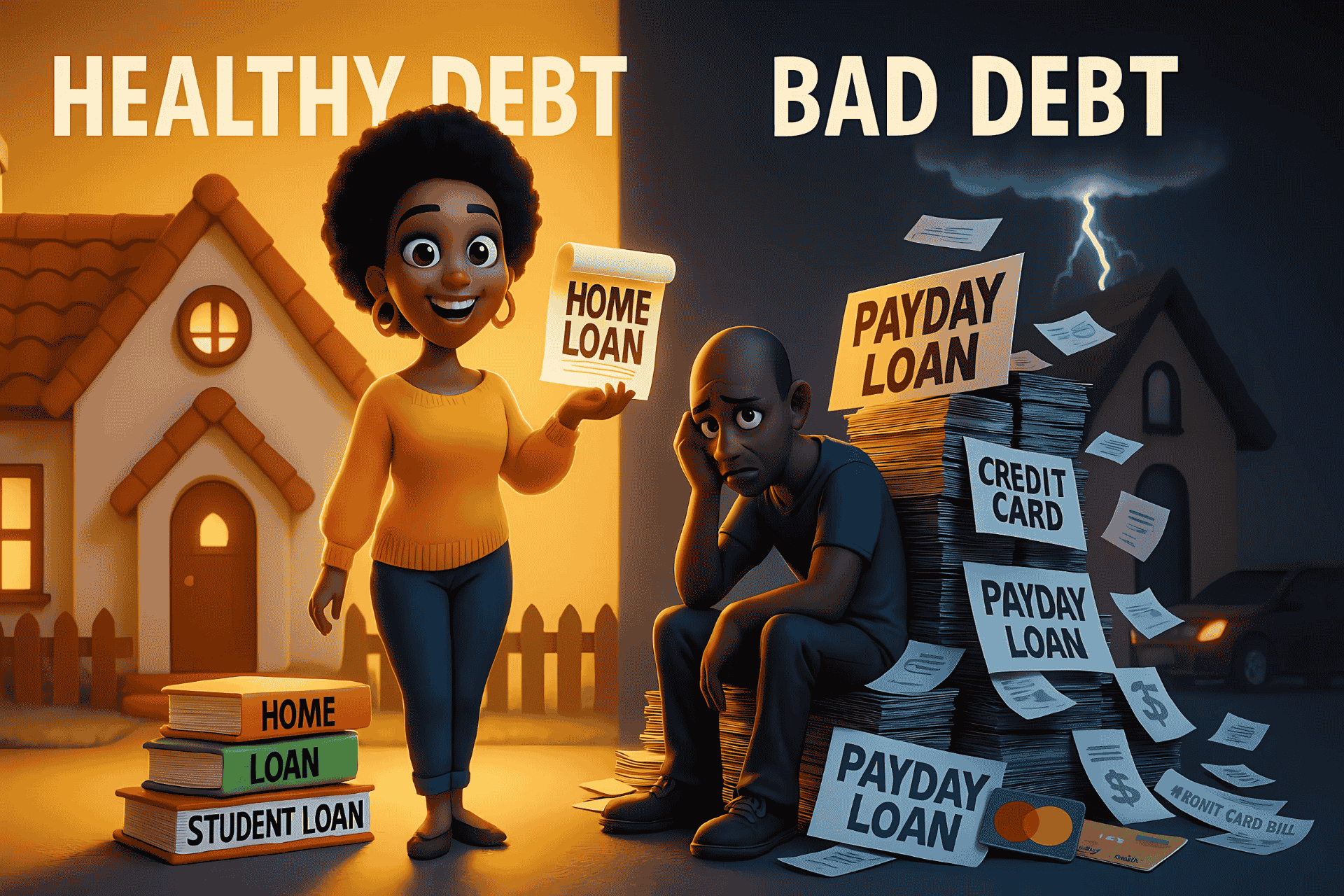

Credit Agreements That Will Not Form Part of Debt Review

While debt review is comprehensive, it does not cover all types of credit agreements. Understanding what is included and excluded helps set realistic expectations about the process.

Included in Debt Review:

- Personal loans.

- Credit card debt.

- Vehicle finance.

- Store accounts.

- Home loans.

Excluded from Debt Review:

- Short-Term Debts: Debts like payday loans may fall outside the debt review process, depending on their terms.

- Unsecured Debts Not Disclosed: Any debt not reported to the Debt Counsellor cannot be included in the repayment plan.

- Future Debts: New credit agreements taken out after initiating debt review are not included. However, such agreements will be prohibited by means of placing a debt review flag on your credit record, thereby precluding you from entering into further credit agreements.

- Legal Action: Legal action may have already taken place on credit agreements which have been in default for some time. If you have received a letter of demand for a certain account in arrears, the account can still be included in Debt Review. However, if a summons to court has already been received on an account in arrears, you still can enter the Debt Review process even though the account in question will not form part of the Debt Review process.

It is essential to provide a complete picture of your financial obligations when applying for debt review. This ensures your repayment plan is comprehensive and realistic.

Best Time for Debt Free Is Now

There’s no perfect moment to seek debt help; the best time is always now. Waiting for your financial situation to worsen can limit your options and make recovery more challenging. Debt review is not just about paying off debt; it’s about taking back control of your life.

Benefits of Starting Now:

- Immediate Relief: Stop creditor harassment and legal action right away.

- Protect Your Assets: Secure your home, car, and other essential belongings.

- Build a Better Future: The sooner you start, the sooner you can enjoy financial freedom.

Remember, debt relief isn’t just about escaping debt; it’s about creating a sustainable financial future. The debt review process empowers you to move forward with confidence and clarity.

Conclusion

Understanding when to enter the debt review process can be the difference between financial stability and continued struggle. Whether you’re facing letters of demand, defaulting on payments, or struggling to make ends meet, debt review offers a legal and structured solution. By acting early and consulting a trusted Debt Counsellor at DebtCut, you can protect your assets, rebuild your credit, and achieve lasting financial freedom.

Don’t wait until it’s too late. The best time to take charge of your finances and embrace a debt-free life is now. Contact a registered Debt Counsellor today or make use of the website tools and begin your journey toward a brighter, stress-free future.

Discover Your Debt Relief Solution

Learn more about our debt relief services today

Read More of Our Latest Blog Posts

We take care to bring you only the highest quality information, right to your fingertips. Read more below:

Satisfied Customers

Read what our customers have to say about us.

"Thank you DebtCut! Thank you very much! You helped me take care of my family. I will not make debt again."

"DebtCut gave me a second chance. I was in so much debt that I couldn’t see a way out. With debt review and over time, I cleared all my debts. It’s a disciplined process, but it works!!”

Take Control of Your Finances Today!

Contact DebtCut today to learn how we can help you achieve financial freedom.